By Greg Smith

Pretty much everywhere you look at the moment the messages appear to be all about economic doom and gloom. The prices of food, petrol and many other essential goods continue to rise, putting pressure on consumer wallets. House prices are falling all over the country, with further salt being rubbed in the wounds by rising mortgage-rates, giving those who are coming (or about to come) off lower one-year fixed year deals a nasty shock.

Meanwhile many commentators and economists extol (almost gleefully in some cases) that the Kiwi economy is already in recession. Unemployment is at record lows, exporters are doing well, and borders are opening up, but economically, things are to only get tougher it seems. The message is that it is time to batten down the hatches (apart from the government, which has continued a massive spending splurge).

Then there’s the stock market. Emotive headlines always garner the most attention so it should not surprise that when kiwi shares recently went into a ‘bear market’ (falling 20% from last year’s peak) not long ago, it captured much media attention. The NZX50 has though rallied somewhat in recent weeks, but is still hovering around ‘bear market” territory, with the decline from the January 2021 high still around 20%. It has nonetheless been a ‘volatile’ first half of the year. The NZX50 lost 3.8% for the month of June and is around 16% lower in the first six months of 2022.

We are not alone.

Indeed, US markets have had a tougher time of it. The tech laden Nasdaq is down 30% year to date, while the broader S&P500 has had its worst first half of the year since 1970. Volatility has been the highest since 1932, around the time of the Great Depression. The bond market has been even worse, recording its weakest start to the year since 1788!

Some perspective is perhaps needed.

This year has been one when markets globally have repriced in higher levels of inflation and the interest rate tightening that has come with it. After unprecedented levels of stimulus during the pandemic, the “punch-bowl” has had to be taken away. The piper has to be paid. The war in the Ukraine has of course greatly exacerbated matters as it relates to the inflationary pressures the world was already facing.

The speed of the market’s decline jumps out, as investors have quickly come to the view that inflation will be with us for some time, and the ultimate outcome will be a recession. With markets pricing in the worst, this therefore lends itself to the question - what happens if the bear-case scenario is avoided?

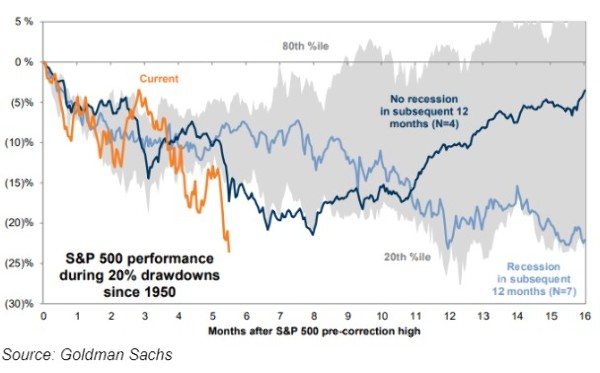

The below chart shows the performance of the S&P500 in the US since 1950 when a 20% drawdown in the index was followed by a recession (lighter blue line), and also in the times when it wasn’t (darker blue line). Perhaps unsurprisingly, when a recession was avoided, the market performed strongly on the upside.

Whether we will get a recession this time around remains to be seen, but history has shown that during these periods markets are prone to pricing errors. This can create opportunities for active stock selection strategies (such as those used by Devon). Further, there will be some companies and sectors that can perform well, even in event of a downturn.

Inflation outcomes clearly hold a massive key. Think back to last year when inflation was seen as ‘transitory.’ Central banks then pivoted to the notion that inflation was set to endure a little while longer. The matter was then thoroughly put to rest by the situation in Ukraine which saw prices for a host of commodities accelerate to the upside.

A tight labour market is driving wages higher, which has sparked notions of a 1970’s wage price spiral. A key difference however was that 50 years ago it was all about supply side disruption (and the oil shock). This time around, while supplies have been interrupted it is also arguably more about the demand side, as the world reopens post Covid.

Markets have been uber-sensitive to inflation prints, which generally speaking have been coming out ahead of expectations more often than not. Simple mathematics however tells us that we are likely close to topping out in terms of the size of the year-on-year inflation numbers being seen. The risk therefore is that inflation begins to soften, central bank responses are potentially moderated, and we ultimately see a more balanced set of probabilities over whether various economies do go into recession.

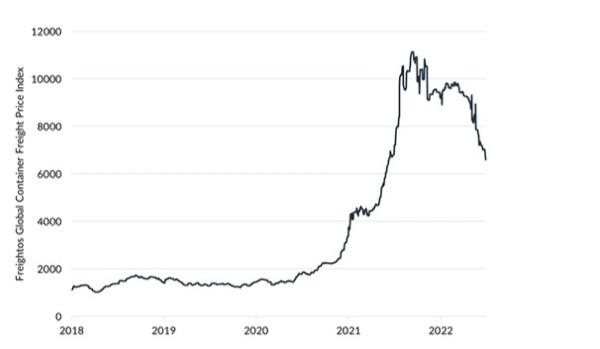

Inflation has already softened in a number of areas. Shipping rates have been a hot topic during the pandemic with these surging due to supply chain blockages, and ultimately having been passed onto consumers. As the chart below shows, these are well down from their highs as congestion has started to ease. While high prices for many commodities are linked to the war (the timeline for which is unknown), there is cause to believe that the global reopening will continue to take some of the heat out of inflation elsewhere.

Looking at recession probabilities amongst global economies, New Zealand’s is clearly a big risk, particularly given the quantum of our short-dated mortgage debt. Surging house prices were a feature during the pandemic amid ultra-low borrowing rates. Although there has already been a retracement there is also arguably much further for NZ house prices to fall (a recent Bloomberg Economic report cited our market as being the most at risk on the basis of price to income ratios and general affordability).

Falling house prices have a knock-on wealth impact to consumer spending, which is already being increasingly pressured by the rising costs of living, and higher borrowing costs as people come off shorter term mortgages. This has a direct flow though to the economy, with consumer spending accounting for around 70% of GDP. The rest of the world is arguably more ambiguous.

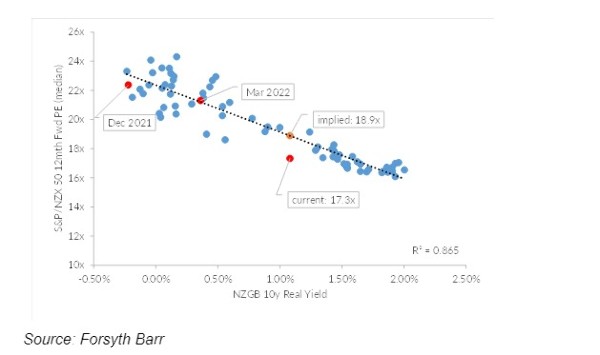

Bringing it back to markets however, a lot of bad news has already been priced in. Much has been made of the fact that rising bond/interest rates are making equities look less appealing. However, the correlation between the PE of the NZX50 and the real yields on 10-year government bonds has been fairly tight over time. At current rates the implied P/E (price-to-earnings ratio), based on this historical analysis for the NZX50, is around 18.9x. It currently is sitting at 17.3x, which all else equal suggests that equites are becoming supported by their valuation.

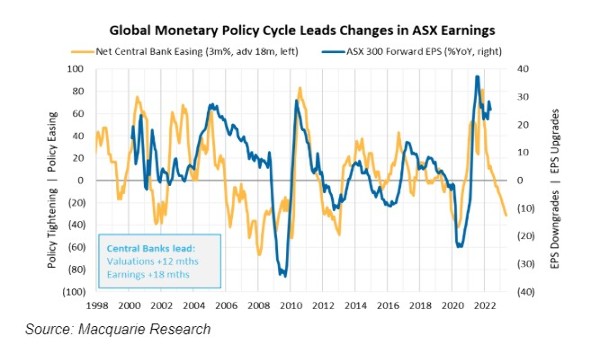

Ultimately the big question now though is what happens to corporate earnings - the ‘E’ within P/E. History shows that earnings will be impacted as central banks tighten and economies slow. To demonstrate this relationship, the chart below tracks the correlation between monetary policy and earnings on Australia’s ASX. This should ultimately drive markets over the next six months or so.

A key question though is just how long the central bank tightening experience endures. We know full well that most central banks are resolute in their quest to bring down inflation to the extent they can. At the same time officials will also not want to send economies into a tailspin. Fed Chair Jerome Powell has recently commented that the Fed could well change tack if the economy were to stutter. The RBNZ has yet to employ this language, but where the Fed goes others tend to follow.

Either way this could mean that the tightening process endures over a shorter timeframe than is currently priced in by markets – either because the economy stutters, or inflation is brought under control quicker than expected.

History has also shown that once central bank tightening processes start, longer term bond rates tend to stabilise. This is important because of the debt that exists in the system. We do hear much about the challenges around debt levels which are elevated here, and in many other countries globally. Although these concerns are certainly relevant, it is worth highlighting that over the past few years household savings rates lifted materially as people were affected by Covid and related policies. The underlying economic environment therefore may not be quite as fragile as the headlines would suggest.

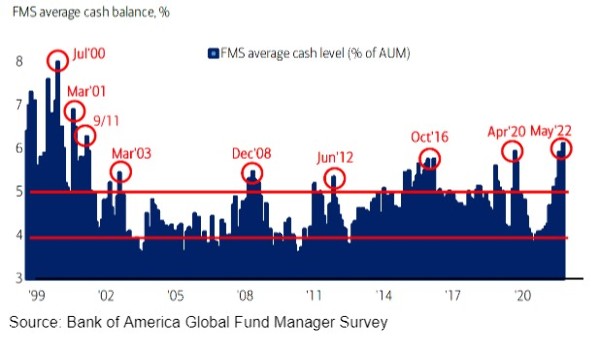

Back to markets, focusing this time on the subject of cash. This is also very high from the perspective of fund managers. A recent Bank of America survey shows that the cash levels of long only managers globally is the highest since 2001. A lot of investors have therefore already positioned for the volatility that we are seeing.

The highest level of cash held since 9/11!

The point of this observation is to highlight that there is only so much more selling that can be done by investors. Managers also haven’t been this underweight the equity market since April 2020 when Covid hit in earnest. Pessimism is high, but markets also tend to turn at bearish (and bullish) extremes.

Is the fork in the road close at hand?

Time will tell, but a “lot of work” has already been done on the downside in response to the inflation and economic frailties, in terms of these factors being priced into the market. Such an environment is arguably very productive for active investors that are selective about stocks and sectors. Less so for passive ones.

At Devon our funds have navigated this year’s volatility well. We have stayed true to our valuation disciplines and focused on high quality, ‘real’ companies. We are happy to pay for growth, but only at the ‘right’ price. This has underpinned a strong market relative investment performance across our funds.

Clear valuation propositions continue to emerge, which has seen our Devon Alpha Fund move from around 25% cash a month or so ago to half of that currently. Although market volatility will remain a feature over the next few months, the opportunity for investors is improving. A rising tide though may not lift all boats.

Comments

No comments yet.

Sign In to add your comment